A Case Study of Navy Yard Building 101

Original research by Jacqueline M. Jenkins, University of Pennsylvania Wharton Small Business Development Center

Introduction

CBEI researchers used Building 101 to examine the variability in energy audits among three service providers, and explore the effect that this variability has on building owners who are considering energy efficient retrofits. The data available from the highly instrumented Building 101 was used to assess audit accuracy and develop suggestions for increasing standardization of the auditing practices and data analysis.

Building 101 at the Philadelphia Navy Yard

Building 101 in The Navy Yard was the temporary headquarters of the U.S. Department of Energy’s Consortium for Building Energy Innovation (CBEI). The building is currently owned by the Philadelphia Industrial Development Corporation (PIDC) and managed by Cushman and Wakefield.

Built in 1911, Building 101 was originally a Marine barracks at the The Navy Yard in Philadelphia. All of the building’s mechanical systems were updated in 1998. The building is currently used as an office building with multiple tenants, including PIDC, and various commercial tenants.

Building 101 covers 61,700 square feet over four floors (basement through third floors). The building is in the shape of a “T” with three wings, and is comprised of offices, a lunchroom, mechanical spaces, and miscellaneous support spaces, as well as a lobby/atrium located in the center of the building. Tenant space is located in all four floors, including the basement. Mechanical equipment lies in the basement mechanical rooms and the attic, which is also used for storage. Building 101 is occupied throughout the year, with typical office hours for office spaces.

Building 101 Energy Efficiency Opportunity

The Building 101 instrumentation project is determining a baseline for energy use in the building. Ultimately, the building will be used as a test bed in which the effectiveness of a new building system can be measured against this baseline. The ability to establish the precise impact of a discrete building system will be an excellent resource for the regional market.

As one of the nation’s most highly instrumented buildings, Building 101 streams over 1,500 data points every 60 seconds. This data reflects the energy, comfort, and indoor air quality (IAQ) baseline, which will be used to calibrate and verify detailed simulation models of the building systems, as well as to quantify the impact of any improvements.

Using this instrumentation data, EEB Hub researchers tested the efficacy of energy audits, one of the first steps in a building retrofit. They contracted three energy auditing firms with distinct audit practices to survey the building and report on energy use and costs, as well as to make recommendations for upgrades and renovations.

The Energy Audit Process

Energy auditing is a systematic process for analyzing a building’s existing energy usage and identifying opportunities to conserve energy and achieve energy cost savings. It is common practice to perform an energy audit when planning either a major energy efficiency renovation or adapting the use of a building. Three levels of energy audits are generally recognized by auditors, with level I and level II audits being most commonly used.

- Level I: A simple walk-through inspection by an “experienced observer” leading to verbal recommendations

- Level II: An analysis of the detailed energy use of a building, attributed to the various building subsystems, followed by a financial analysis of best return on investment for building or system upgrades

- Level III: A deeper investigation, focused on a whole-building computer simulation, of the retrofits identified in the Level II audit that require significant capital investment.

Level I is used to determine a rough estimate of efficiency improvements and/or to help identify capital projects. Level II offers specific recommendations and investment costs and is the most commonly utilized audit, while level III is a detailed analysis of capital intensive modifications.

These definitions leave some room for interpretation. Each individual engineer might draw the line between Level I and Level II services differently, and the client often influences an auditor’s priorities, making the levels somewhat subjective.

EEB Hub researchers expected the results of the three firms to be fairly consistent. Conversely, each Energy Audit firm presented very different findings and recommendations.

Building 101 Energy Audit Results

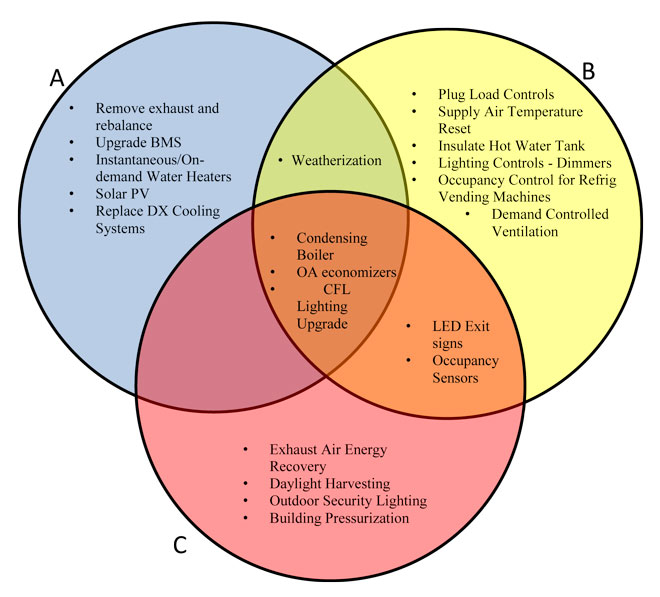

Company A: Overview of Findings and Recommendations

Company A’s engineering staff visited the site in October 2011. The audit team inspected Building 101’s office areas, common areas, mechanical equipment rooms, and building envelope. Sampling rates of equipment and spaces were determined in the field. The audit team inspected all of the air handling units (100% sample rate) including supply fan motors, dampers, coils, and valves, with the testing methodology focusing on equipment relevant to specific energy conservation measures (ECMs).

Company A identified ten ECMs, including: disconnect exhaust fan, envelope/door weatherization, lighting upgrades, building management system, air-side economizer, tankless water heaters, solar panels, condensing boiler, replace direct expansion cooling systems, and increased attic insulation.

Company A contended that, if all of these ECMs are implemented, they would provide a total annual electric and gas cost savings of $60,200 (38% savings).

Company B: Overview of findings and recommendations

Company B surveyed the facility including the lighting systems, windows, insulation levels, domestic hot water systems, HVAC systems, and controls, plus performed a detailed utilities analysis. Company B then developed a calibrated energy simulation computer model and performed various “what-if” scenarios in order to develop their recommendations. Company B’s approach was meant to be quick, but accurate, using the structured energy auditing software kW-Field.

Company B recommended six ECMs: airside controls optimization, building pressurization, exhaust air energy recovery, replacing boiler with staged condensing boilers, lighting controls and retrofits, occupancy sensors, emergency lighting fixture schedules, daylight harvesting, T12 to T8 lighting fixture retrofit in restrooms, and retrofit outdoor security lighting.

Company B’s analysis indicated that approximately $22,495, or 14.5% of the present utility costs, could be saved by implementing these ECMs.

Company C: Overview of findings and recommendations

Company C analyzed Building 101 and proposed fourteen ECMs, eight of which involved lighting and lighting control upgrades. Other ECMs proposed include: re-commission of building envelope; installing plug load controls; mixed and supply air temperature reset; replacing the conventional natural gas boiler with a new condensing gas boiler; economizers on rooftop units; and hot water tank insulation.

Company C’s analysis suggested that these ECMS could be expected to reduce facility electricity consumption by about 16% and natural gas consumption by about 61%, resulting in $34,000 or 24% reduction in annual utility expenditures.

Audit Variability

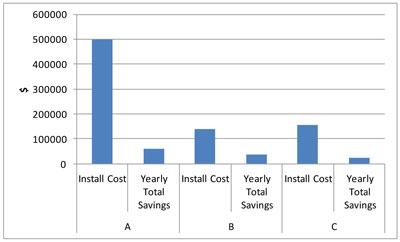

The graph below summarizes the annual savings, implementation costs, and simple payback periods for all three Energy Audit results:

The arrays of Energy Conservation Measures (ECMs) varied significantly among Energy Audits, both in ECM technologies recommended and their prioritization with respect to energy savings impact. Only a few of the same ECMs appear on all three auditor lists and none of those are prioritized in the same way. In addition, the differing naming conventions and categorization of ECMs among firms make precise comparisons difficult.

For example, all three energy audits identify lighting and lighting controls as an ECM. However, Company C identifies eight distinct Lighting ECMs, each with its own implementation costs and payback periods. The total implementation cost is about $8,000, with an average payback period of 4.8 years. Company A, on the contrary, groups all Lighting ECMs into one overarching Lighting Upgrade ECM, with an implementation cost of about $81,000 and a payback of about 4 years. Finally, Company B identifies five distinct Lighting ECMs, with a total implementation cost of about $43,000 and an average payback period of 6.7 years. This variability in recommended measures demonstrates that even within a similar ECM category, different auditing firms may produce disparate proposals and estimates.

Of note, Company C and Company A did offer similar predictions regarding Building 101’s carbon footprint reduction as a result of the proposed retrofits: 199 tons and 205 tons, respectively. Company B did not calculate a carbon footprint reduction estimate based on the firm’s proposed retrofits, which is, in itself, another point of variation among energy auditing processes.

Recommended installation costs and overall yearly savings differed among auditors as well. Company C offered the lowest installation cost of $138,130 and annual savings of just under $40,000. Company A proposed the most expensive initial investment at $497,690, but offered annual savings of approximately $60,000 and with a payback time only 4.6 years longer than company C suggested.

Company A was the only company to identify the benefits and necessity of upgrading Building 101’s Building Monitoring System (BMS) to a BACnet control system (i.e. a system that complies with the BACnet protocol, a standardized set of rules governing the communication of data about building automation and control networks) and included extensive detail on the building’s current BMS. This point explains the much higher expense of Company’s A installation recommendations. In fact, the BMS did have to be replaced before the completion of this case, proving the benefit of upgrading to a new BMS unit as opposed to investing in optimizing the existing controls.

The data gathered by the energy audit firms on quantifiable energy usage and costs, as well as sustainability measures such as carbon footprint, showed much less variability than the firms’ estimates of the costs and payback periods of the proposed ECMs. Thus, much of the variability between firms arises from the estimates of equipment costs and the labor to install that equipment, analogous to three different automobile mechanics diagnosing a similar problem with a car but quoting widely different repair costs based on parts and labor estimates.

Recommendations for Energy Audit Standardization

Standardizing the assessment of a building’s energy use will give building owners and institutions more confidence in the value of energy audits and the building retrofit projects that rely on them. In addition, greater standardization of energy audits could incentivize utility companies to offer energy audits in efficiency incentive programs and would leverage energy disclosure ordinances by providing a standardized first step for owners to improve building energy performance.

To address the problem of variability among auditing practices, CBEI is developing a protocol-based Energy Auditing Process with a set of measurement and modeling tools that will lead to standardization of the Level II auditing process. An introduction to this process is listed below.

The conversation on standardization begins with building a common language. Even the term “energy audit” is commonly misused. Some companies that sell energy products exploit the term “energy audit,” using it to refer to what is actually a sales proposal that recommends products they sell. This practice leads to loss of credibility in the energy audit business. The EEB Hub hopes to eliminate this kind of misapplication by building consensus around the definition of industry terms and around types of documentation expected to accompany any energy audit.

The next step in limiting variability among energy audits is to provide all auditors with a detailed, sequential walk-through protocol. In the case of Building 101, a well-designed walk-through protocol would have aided Company C in identifying that more was needed than simply optimizing the BAS controls and it would have encouraged Company B to provide a carbon footprint reduction estimate. By laying out a logical path through the audit process and calling for in-depth considerations of payback periods, CBEI will promote consistency among ECM recommendations by auditors.

CBEI provides a neutral space to foster collaboration among audit providers in gathering and analyzing data, as well as in marketing and promoting auditing services. Given the robust data that CBEI have already gathered on instrumentation, control upgrades, and the energy audit process, Building 101 can serve as an ideal test bed or control subject for energy audit firms to refine their techniques and study what ECMs are most useful in any baseline energy audit.